%20scale(0.100000,-0.100000)'%20fill='%23000000'%20stroke='none'%3e%3cpath%20d='M1100%2012055%20l0%20-2695%202310%200%202310%200%200%20385%200%20385%20-1925%200%20-1925%200%200%20770%200%20770%201925%200%201925%200%200%20385%200%20385%20-1925%200%20-1925%200%200%20770%200%20770%201925%200%201925%200%200%20385%200%20385%20-2310%200%20-2310%200%200%20-2695z%20M6550%2012060%20l0%20-2690%202690%200%202690%200%200%201535%200%201535%20-1535%200%20-1535%200%200%20-385%200%20-385%201150%200%201150%200%200%20-770%200%20-770%20-1920%200%20-1920%200%200%201925%200%201925%202305%200%202305%200%200%20385%200%20385%20-2690%200%20-2690%200%200%20-2690z%20M1100%205805%20l0%20-2695%20385%200%20385%200%200%20770%200%20770%201073%200%201072%20-1%2075%20-82%20c41%20-45%20360%20-392%20708%20-770%20l633%20-687%20524%200%20c289%200%20525%202%20525%205%200%203%20-109%20124%20-242%20268%20-608%20657%20-1153%201251%20-1156%201258%20-2%205%20314%209%20702%209%20l706%200%200%201925%200%201925%20-2695%200%20-2695%200%200%20-2695z%20m4620%20770%20l0%20-1155%20-1925%200%20-1925%200%200%201155%200%201155%201925%200%201925%200%200%20-1155z%20M7320%205795%20l0%20-2695%202305%200%202305%200%200%20385%200%20385%20-1920%200%20-1920%200%200%20770%200%20770%201920%200%201920%200%200%20385%200%20385%20-1920%200%20-1920%200%200%20770%200%20770%201920%200%201920%200%200%20385%200%20385%20-2305%200%20-2305%200%200%20-2695z'/%3e%3c/g%3e%3c/svg%3e)

Yield analysis · 6 min read

JVC Yield Reality Check: Gross vs Net Returns

Why headline yields rarely tell the full story.

Jumeirah Village Circle has become one of Dubai's most heavily marketed investment sub-markets. For many first-time investors, the appeal is obvious: lower entry prices, strong rental demand, a large tenant base, and headline gross yields that often appear more attractive than prime waterfront or central districts.

But headline yield is not the same as real return.

In JVC, the difference between a broker-quoted gross yield and an investor's actual net return can be significant once service charges, furnishing, management costs, void periods and realistic rental assumptions are properly accounted for.

This is where many investors make their first mistake. They buy the marketing yield, not the operating asset.

At EGRE, we assess JVC opportunities by moving from the advertised number to the actual net return. The question is not simply:

"What is the gross yield?"

The better question is:

"What does the investor actually retain after all recurring costs, vacancy assumptions and exit risk?"

The gross yield trap

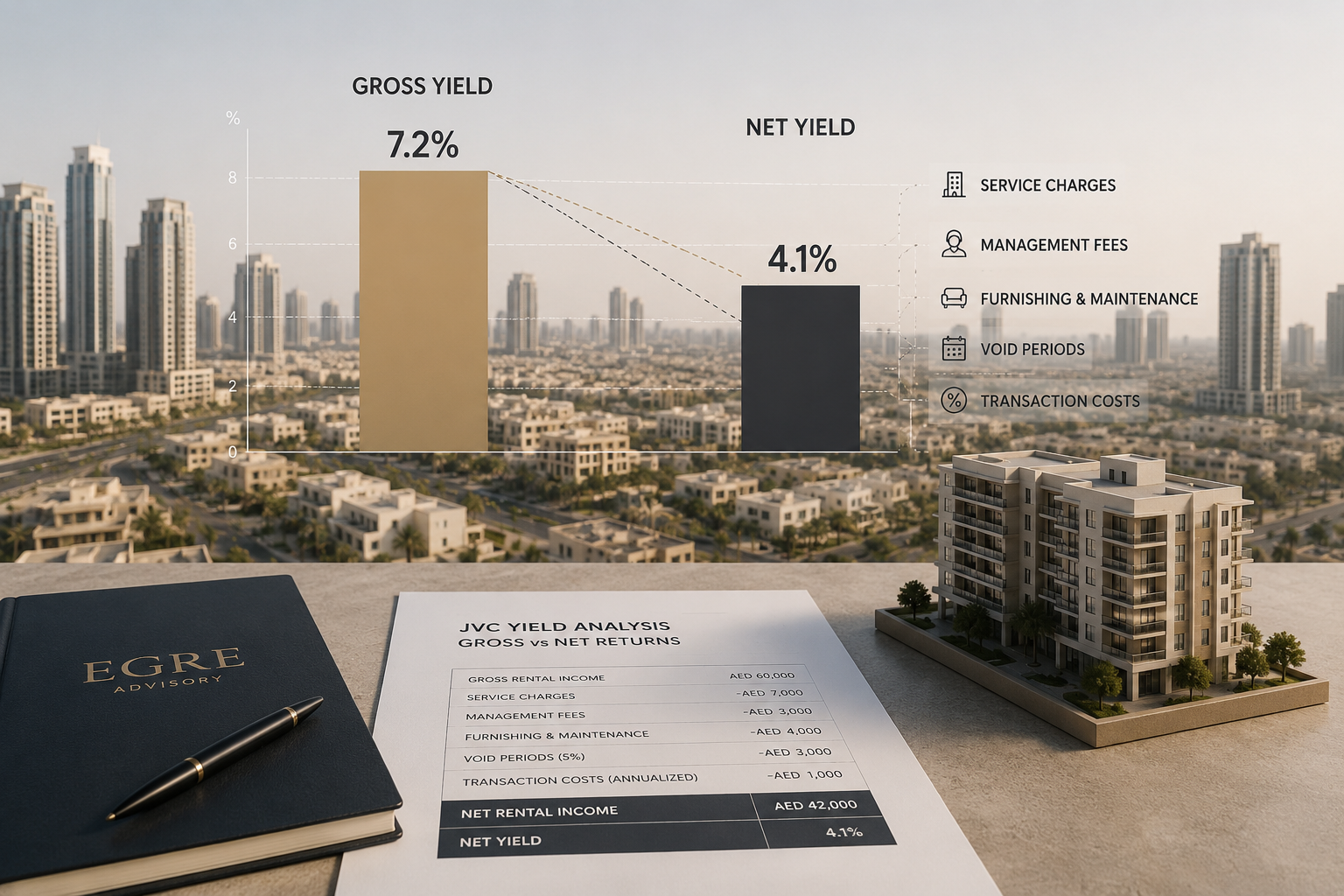

Gross yield is usually calculated using a simple formula: annual rent divided by purchase price.

On paper, that can make JVC look compelling. A lower purchase price combined with a seemingly strong rent can produce a headline yield that looks attractive compared with areas such as Dubai Marina, Downtown or Dubai Hills.

But the issue is that gross yield does not account for the real cost of ownership.

It usually excludes:

- Service charges

- Property management fees

- Letting fees

- Vacancy periods

- Furnishing and maintenance

- Chiller or utility-related obligations

- Transaction costs

- Resale liquidity risk

Once those items are included, the net return can compress materially.

This does not mean JVC is a bad investment. It means JVC needs to be underwritten properly.

Service charges matter

Service charges are one of the most important variables in JVC underwriting.

Two apartments with the same purchase price and rent can produce very different net returns if the service charge profile is different. A building with high recurring charges, weaker maintenance quality or less efficient facilities can erode returns quickly.

This is particularly important in JVC because the area contains a wide range of buildings, developers, specifications and management standards. Not all stock is equal.

A well-managed building with sensible service charges, strong tenant demand and good resale liquidity may still perform well.

A weaker building with elevated service charges, generic stock and limited buyer depth may deliver a far lower net return than the gross yield suggests.

The building matters as much as the district.

Furnishing and management costs are often understated

Many JVC units are marketed to investors as ready rental assets. But in practice, achieving the advertised rent often depends on presentation, furnishing quality and leasing execution.

A furnished apartment may achieve a stronger rent, but furnishing is a real capital cost. It also depreciates over time and may require replacement, repair or refresh between tenancies.

Management costs also need to be included. For overseas investors, especially Chinese or international buyers, professional management is usually not optional. It is part of the operating model.

That means the return should be assessed after:

- Letting and renewal fees

- Ongoing management

- Maintenance coordination

- Tenant communication

- Vacancy handling

- Compliance and documentation

A property that looks simple on a spreadsheet can become far less attractive once the operating burden is properly priced.

Void periods change the real return

The strongest underwriting mistake is assuming 12 months of uninterrupted rent.

In reality, even good rental properties experience gaps: tenant changeovers, maintenance periods, pricing adjustments or leasing delays. In a supply-heavy sub-market, void risk becomes even more important.

JVC has strong rental demand, but it also has substantial competing stock. Tenants have options. That means pricing, building quality, furnishing, location within JVC and unit layout all affect leasing speed.

A realistic model should include a void assumption rather than assuming perfect occupancy.

Even a short vacancy can reduce annual net return meaningfully, especially when the investment case relies on yield.

Why building selection is critical in JVC

JVC should not be analysed as one uniform market.

A good unit in a strong building can perform very differently from a similar-sized unit in a weaker building nearby. Investors need to look beyond the district-level narrative and assess each building on its own merits.

Key questions include:

- What have comparable units in the same building actually rented for?

- What have similar units sold for in recent DLD transactions?

- How many competing units are currently listed?

- Are rents rising because of genuine demand or temporary shortage?

- Are service charges proportionate to the building quality?

- Is there real end-user or investor resale demand?

- How long does stock typically sit on the market?

This is the difference between buying "JVC exposure" and buying a properly underwritten asset.

Gross-to-net compression

The main issue in JVC is not that yields are unattractive. It is that gross yields are often presented without sufficient context.

A property marketed at a strong gross yield may compress once costs are applied. For example, after service charges, management, void assumptions and furnishing costs, a headline yield can reduce materially.

That compression is not necessarily a reason to avoid the deal. But it must be understood before purchase.

If the net return remains attractive after conservative modelling, the opportunity may be worth pursuing. If the investment case only works under perfect assumptions, the buyer is taking more risk than the marketing material suggests.

EGRE view

JVC remains one of Dubai's most active and accessible investment sub-markets. It offers liquidity, tenant demand and a lower entry point than many prime districts.

But it is also a market where selectivity matters.

The best JVC investments are not simply the cheapest units or the ones with the highest advertised yields. They are the assets where entry price, rentability, service charges, building quality and exit liquidity align.

For investors, the discipline is simple: do not buy the headline yield. Underwrite the net return.

At EGRE, every JVC opportunity is assessed through a realistic operating model before it is presented to clients. We look at achieved rents, service charges, comparable transactions, competing stock and resale liquidity to understand whether the investment case holds after costs.

In a market where gross yields are easy to advertise, net returns are where the truth sits.